Steady Nickel

The Dividend Snowball Blueprint

The Dividend Snowball Blueprint

Couldn't load pickup availability

Build a dividend portfolio that pays you, starting from whatever balance you have today.

This is a step-by-step guide to building a portfolio that generates real income from dividends: actual payments deposited into your account, from companies that share their profits with the people who own their stock. You will learn what dividends are and how they work, how to evaluate the funds that pay them, how to build a starter portfolio at your current balance, and how to set up the system that makes the snowball roll on its own.

No jargon walls. No "just buy SCHD" without explaining why. No assuming you already know what a payout ratio is. If you have a brokerage account and money you want to put to work, this guide meets you where you are and walks you through every decision.

What is inside

The Dividend Snowball Blueprint is a 43-page PDF guide with seven sections that build on each other:

What dividends actually are (and are not). Most beginners confuse dividends with free money. This section explains what is really happening when a company pays you, why the stock price drops on ex-dividend day, and why "passive income" is a useful but misleading label.

The yield trap. The single most expensive mistake in dividend investing is chasing high yields. This section teaches you why an 8% yield is usually a warning signal, not a buying signal, and gives you three checks to spot a trap before you buy.

How to evaluate a dividend ETF. A five-point framework covering yield, dividend growth rate, expense ratio, holdings, and payout streak. You will use this framework to evaluate SCHD, VIG, DGRO, and VYM side by side, and you can apply it to any dividend fund you encounter in the future.

Dividend ETFs vs. individual stocks. When ETFs make sense (almost always for beginners), when individual dividend stocks might make sense (later, as a small allocation), and how to tell the difference.

Building your starter dividend portfolio. Three concrete portfolio models at three different starting balances: $500, $5,000, and $50,000. Each model names the specific funds, shows the exact dollar allocation, and projects your annual and monthly dividend income.

The snowball math. A 10-year projection showing how a $500 portfolio with $50/month contributions grows from $17.50/year in income to over $520/year. This is the section that makes the first three years feel survivable.

What to expect in years 1 through 3. The three emotional traps (disappointment, frustration, panic) that cause most beginners to quit, named in advance so they lose their power. Plus tax considerations, what to ignore for now, and a section on the DRIP decision.

What you walk away with

A dividend portfolio plan tailored to your current balance ($500, $5,000, or $50,000), with specific fund allocations and projected income.

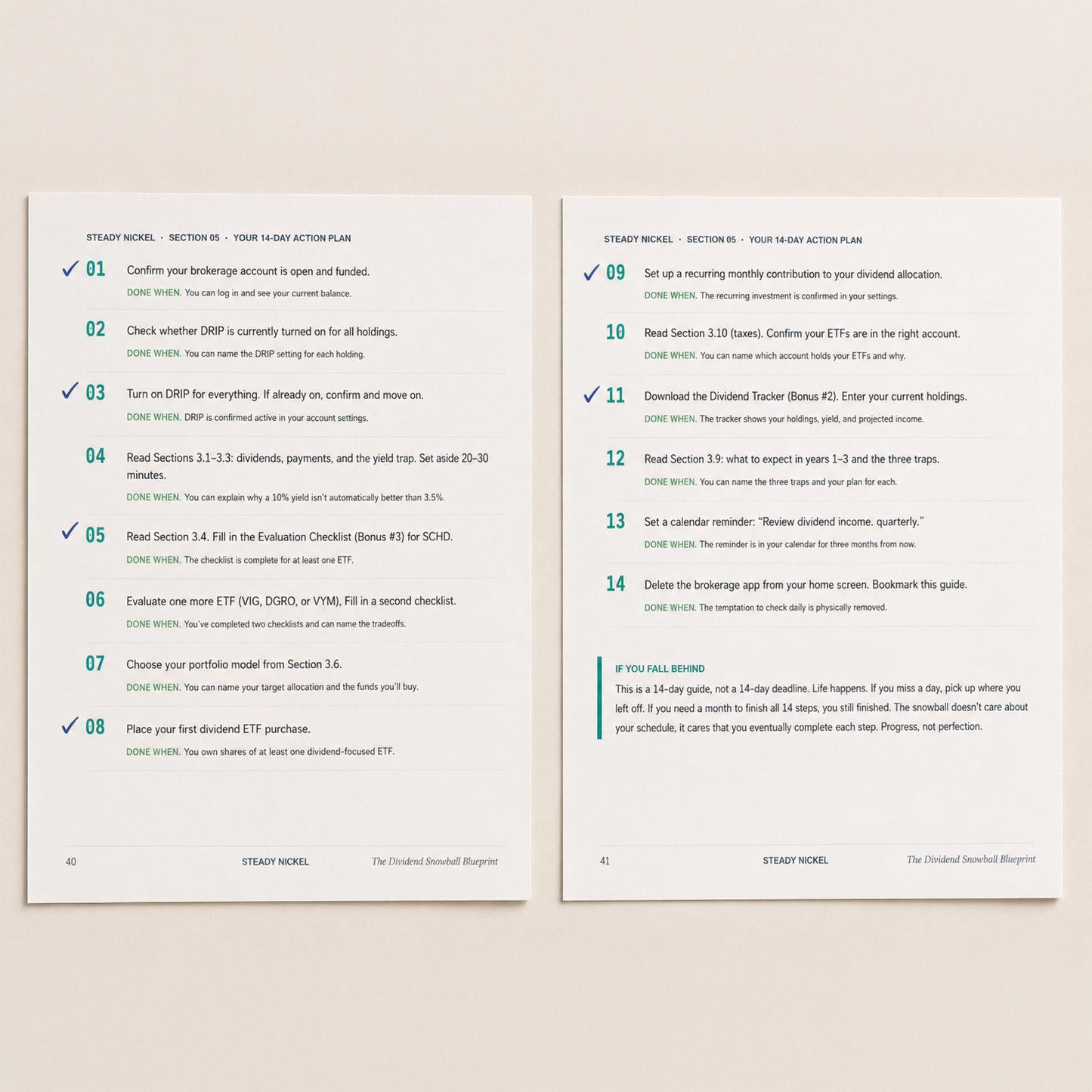

A 14-day action plan with day-numbered steps and "Done when..." checkpoints so you know exactly what to do and when you have done it.

A Dividend Snowball Cheat Sheet (separate PDF): a one-page printable reference with the ETF comparison table, yield trap red flags, and a "what to ignore" list. Print it. Tape it next to your monitor.

A Dividend Tracker (Google Sheets template plus printable PDF): enter your holdings and it calculates current annual income, monthly income, and projected income at 1, 3, 5, and 10 years based on each fund's dividend growth rate. The projection column is what sets this apart from free trackers.

A Dividend Stock Evaluation Checklist (separate PDF): a one-page fill-in-the-blank version of the five-point evaluation framework. Print several copies. Use one every time you are considering a new holding.

Who this is for

Someone investing $500 to $5,000 who wants to understand dividends, build a dividend portfolio, and set up a system that grows their income over time. You may have heard of SCHD or dividend ETFs but are not sure how to evaluate them or where to start. You already have a brokerage account open (or an existing portfolio of index funds) and want your money to start earning income, not just growing in the background.

If you have completed The $100 Portfolio or have an existing portfolio, this is your natural next step. Section 3.6 also includes a plan for balances up to $50,000.

Who this is not for

Active traders, people chasing 10%+ yields from speculative stocks, or anyone who has not yet opened a brokerage account. If you are starting from zero, begin with The $100 Portfolio and get your foundation in place first. This guide assumes you have a funded brokerage account and understand what an ETF is at a basic level.

How it works

After purchase, you will receive an instant download link. The guide is a PDF that opens on any device: phone, tablet, or computer. No special software needed.

Your purchase includes four files:

- The Dividend Snowball Blueprint (main guide, 43 pages, PDF)

- Dividend Snowball Cheat Sheet (1 page, PDF, printable)

- Dividend Stock Evaluation Checklist (1 page, PDF, printable)

- Dividend Tracker (Google Sheets "Make a copy" link, plus a printable PDF version)

The guide is designed to be read in about 60 minutes and completed over two weeks using the 14-day action plan. Each day has one action and one checkpoint. You do not have to do one day per calendar day. The sequence matters. The speed does not.

Read time: ~60 minutes. Complete in: two weeks. Format: PDF + Google Sheets. Updated: June 2026.

Our promises to you

These are not disclaimers buried in fine print. They are features.

No Affiliate Links. We do not earn commissions from any product, platform, or brokerage we mention. When we recommend SCHD, VIG, or any other fund, it is because the data supports it, not because someone pays us.

No Upsell Funnels. Every product is a one-time purchase. There is no hidden subscription, no surprise charges, and no "premium tier" that locks away the important parts.

No Profit Promises. We will never tell you investing will earn you a specific percentage. Dividends can be cut. Markets drop. This guide teaches you how to build a sensible dividend portfolio. It does not guarantee any specific outcome.

No Flexing. You will never see screenshots of our portfolio, net worth claims, or luxury lifestyle imagery. Our credibility comes from the quality of our guides, not the size of our bank account.

Updated Annually. This guide includes an "Updated June 2026" stamp. When fund data changes, brokerage features shift, or tax rules update, we update our guides. For free.

$25. One-time purchase. Yours forever.

Less than a dinner out for two. Less than a month of streaming subscriptions combined. Less than a single hour with a financial advisor.

Frequently asked questions

Do I need investing experience to use this guide? Some. This guide is built for people who already have a brokerage account open and funded. If you have never invested before, start with The $100 Portfolio to get your foundation in place, then come back to this guide when you are ready to add dividend income to your portfolio.

Is $500 really enough for dividend investing? Yes. The $500 Starter portfolio in this guide uses a single ETF (SCHD) and generates roughly $17.50/year in dividend income with DRIP on. That number grows every quarter. The guide includes a 10-year projection showing how $500 with $50/month contributions becomes over $11,400. Every balance starts somewhere.

Which ETFs does the guide cover? Four: SCHD (Schwab U.S. Dividend Equity ETF), VIG (Vanguard Dividend Appreciation ETF), DGRO (iShares Core Dividend Growth ETF), and VYM (Vanguard High Dividend Yield ETF). Each is evaluated using the same five-point framework, and a side-by-side comparison table is included in both the guide and the Cheat Sheet.

What if I have more than $5,000? Section 3.6 includes a $50,000 "Established" portfolio model with a four-position allocation including individual dividend stocks. The framework scales to any balance.

I already own VTI or VOO. Do I need to sell those to follow this guide? No. The guide explicitly addresses this. If you already own broad index funds, you are already receiving dividends (most people do not notice because the yield is low). This guide teaches you how to add dividend-focused holdings alongside your existing core, not replace it.

I already own The $100 Portfolio. Is this the right next step? Yes. The Dividend Snowball Blueprint is designed as the natural progression after The $100 Portfolio. You have a brokerage account, you own index funds, and now you are ready to make your money generate income. The guide picks up where The $100 Portfolio leaves off.

Is this a physical book? No. This is a digital download. You will receive a PDF guide, two one-page PDF bonus files, and access to a Google Sheets dividend tracker immediately after purchase. No physical item will be shipped.

Can I print the guide? Yes. The entire guide, cheat sheet, evaluation checklist, and tracker are designed to be printable on standard 8.5" x 11" paper. The cheat sheet and checklist are specifically designed to be printed and reused.

Will this tell me exactly which stock to buy? The guide covers four specific dividend ETFs in detail (SCHD, VIG, DGRO, VYM) and provides three portfolio models built from those funds. It does not recommend individual stocks by name. Instead, it gives you a framework for evaluating any dividend stock or ETF yourself. The framework outlasts any single recommendation. This is education, not financial advice.

What about taxes on dividends? Section 3.10 covers the basics of qualified vs. ordinary dividends, the tax brackets that apply, and the decision of where to hold your dividend ETFs (Roth IRA vs. taxable account). The guide gives you enough understanding to make a reasonable first decision. It is not a replacement for a tax professional.

What is the refund policy? 14-day refund, any reason. Email us at hello@steadynickel.com with your order number. We will process the refund within 3 business days. You keep the file.

How is this different from free dividend content on YouTube or Reddit? Free content teaches you ideas in scattered pieces. One video says buy SCHD. Another says SCHD is overrated. A Reddit thread recommends chasing 8% yields. Another warns against it. This guide gives you a sequenced system: what to learn first, how to evaluate, what to buy, how to set it up, and what to expect afterward, with clear checkpoints so you know when each step is done. No hunting through 50 videos trying to piece together conflicting advice.

File details

Format: PDF (main guide + cheat sheet + evaluation checklist) and Google Sheets (tracker)

Pages: 43 (main guide) + 1 (cheat sheet) + 1 (evaluation checklist) + tracker

File size: approximately 8 MB total

Compatibility: opens on any device (phone, tablet, computer)

Printable: yes, all files designed for 8.5" x 11" paper

License

This is a personal-use license. You may print copies for yourself and your household. You may not resell, redistribute, or share the files publicly. If someone you know wants a copy, send them to this page.

Refund policy

14-day refund, any reason. Email us at [your email address] with your order number. We will process the refund within 3 business days. You keep the file.

This is education, not financial advice. Past performance does not equal future results. Steady Nickel is not a registered investment advisor. Dividends can be cut and markets can decline. Consult a qualified professional before making investment decisions.

Share